Burns Singh Tennent-Bhohi, Founder and Executive Chairman, outlines Eastport Ventures’ principal mineral assets and plans to achieve a public market listing.

Q&A WITH BURNS SINGH TENNET-BHODI, EASTPORT VENTURES

Please introduce us to Eastport Ventures, the six mineral projects it has strategically acquired over the past seven years, and the company’s multi-million-dollar investment arm.

Burns Singh Tennent-Bhohi, Founder and Executive Chairman (BSTB): Eastport Ventures (Eastport) was founded with the objective of building an innovative and creative mining house that would stand out in a sector devoid of access to capital and suffering from depressed sentiment, which has led to many companies capitalising for their survival as opposed to the development of their mineral assets.

Since its inception, Eastport has evolved to be a well-structured Canadian mining house with exposure to material mineral assets in Botswana.

These licences have benefited from around CAD$18 million in historic and current exploration and development expenditures, which provide the company and its shareholders with exposure to a suite of commodities including copper, rare earth elements, uranium, nickel, and diamonds.

These commodities are critical to international efforts to rebalance the impact of deglobalising economies and trade, whilst concurrently aiding in the electrification of the world in what is the most ambitious energy transition our planet has seen in the last century.

In addition to generating direct exposure to these sought-after commodities, the company has quietly built a venture arm that has to date generated a return, at peak, in excess of 100 times the capital invested.

Core to Eastport’s strategy has been patience and sacrifice. Over the past five years, our co-Founder, Rick Bonner, and I have instilled a lean operating model with a solid corporate ethos that ensures all capital raised is applied to the development and growth of the company.

One of our core principles is that whilst Eastport has remained a private company, none of our directors have taken any form of compensation, nor have they received any free equity as we gear up to our public listing. This is a rare and unique approach, but one which has galvanised a group of directors and senior managers who collectively have over a century of experience operating in this industry.

Our board have complementary skillsets that cover all key areas necessary for operating a company of this nature. During the preceding challenging years, we have remained focused on our present objective, which is to drive our assets through the value chain to a point of materiality that we feel is befitting of greater and broader capital markets participation.

For a long while, I have been disillusioned with the conventional approach adopted by the sector for exploration and development companies to rely disproportionately on capital markets to finance the highest degree of risk, which sees dilution through equity and a reliance on market sentiment take effect long before investors are exposed to a drill bit.

At Eastport, we have worked diligently to advance one or more of our assets to a drill-defined status, and by meeting this objective, a key criterion has been achieved in order to proceed with listing on a recognised investment exchange.

Now, with all permits in hand, we can provide market participants with immediate exposure to years of work that has mitigated associated risk, and in turn ensures investors gain immediate exposure to operational execution and results. Even prior to listing, we have undertaken drilling on our projects, whilst others are either drill-ready or await the conclusion of geophysical interpretation or final drill/environmental permitting.

We believe that achieving this status across our projects represents a powerful and compelling proposition for investors and demonstrates how we want to differentiate Eastport from its peers by driving aggressive optionality across the portfolio. We are proud to have achieved this objective to derisk the proposition for investors prior to a public offering.

“Since its inception, Eastport has evolved to be a well-structured Canadian mining house with exposure to material mineral assets in Botswana”

Burns Singh Tennent-Bhohi, Founder and Executive Chairman, Eastport Ventures

Eastport has a suite of mineral interests. What, in your opinion, are the principal mineral assets within the business?

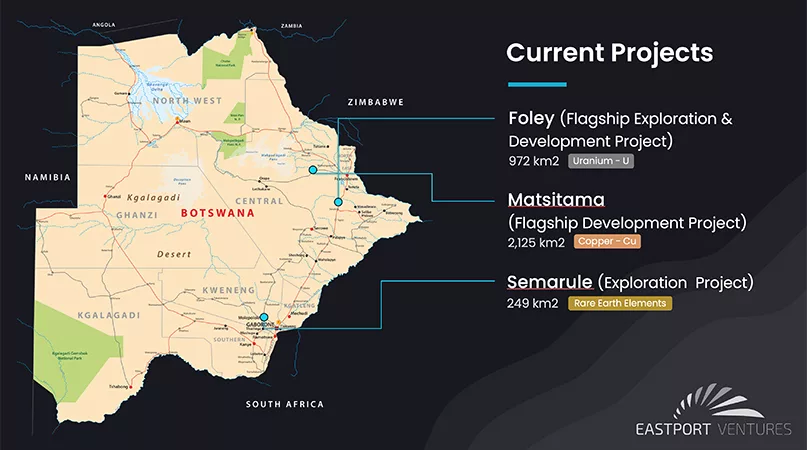

BSTB: The most advanced project in the portfolio is the Matsitama copper project, which is comprised of three known targets – Nakalakwana, Phudulooga, and Lepashe.

Nakalakwana is an advanced-stage target with an indicated and inferred copper resource of 9.9 million tonnes at 0.464 percent.

Eastport’s objective is to increase the known resource of Nakalakwana, bring it up to a code-compliant resource, and to explore for additional resources in proximity.

Phudulooga, meanwhile, is located in close proximity to the Kopano Copper Mine. It has a copper zone that is known to be at least 1,600 metres (m) long by 30m wide and is characterised by high-grade chalcopyrite up to 13 percent.

Eastport’s objective is to better define the extent of the copper zone through a combination of drilling and infill geophysics.

The Lepashe area features widespread anomalous copper mineralisation, with numerous bedrock samples having assayed up to one to two percent copper. Post-listing, Eastport will undertake geochemical and geophysical exploration work.

Aside from the Matsitama project, another key asset is the Foley uranium project, which is located directly to the north of the Letlhakane uranium deposit, which is one of the largest undeveloped uranium projects in the world, now owned by Lotus Resources.

Foley has been derisked through recent historic drilling, which has confirmed the existence and presence of uranium, with elevated grades observed in the assay results.

Importantly, the favourable geologic unit that hosts the Letlhakane uranium deposit extends throughout the Foley project, and the favourable stratigraphic similarities give confidence to our belief that it could host a significant high-grade resource. We look forward to commencing drilling activities at Foley post-listing.

The third project in our portfolio that we have high hopes for is Semarule, which is prospective for rare earth elements. The project hosts an outcropping mineral-rich multi-phase syenite with carbonatite dykes over a three square kilometre (sqkm) area reaching an elevation of 75m above regional cover.

To date, surface rock sampling has reported up to 5,097 parts per million (ppm) total rare earth oxides (TREOs), which compares favourably with other rare earth projects worldwide.

A subset of key light and heavy rare earths including neodymium, praseodymium, and terbium has assayed up to 1,270 ppm. Infrastructure is excellent at the project, and we are excited about its potential.

How does Eastport plan to achieve a public market listing and advance up to three drill programmes across three of its development-ready projects?

BSTB: There are a number of routes open to Eastport to achieve a public market listing in Canada, including a direct listing, a qualifying transaction with a capital pool company (CPC), a reverse takeover (RTO), or an initial public offering (IPO).

My board and I have discussed and considered all options open to the company and look forward to sharing our strategy with the market in the coming weeks.

We have waited patiently for the right market conditions to take Eastport public and believe that the appreciation in the commodity prices of our key metals over recent months, specifically copper, nickel, and uranium, will ensure that market sentiment and investor interest will be supportive of the mining house we have built and the intrinsic value waiting to be unlocked from the point of listing.

Indeed, we have been delighted with the interest shown by leading brokers in Canada, the support they anticipate from investors, and the work programmes we have in place to advance our project portfolio.

What clear vision do you have of how you will work to augment future value for the company and its shareholders?

BSTB: Commodity prices are inherently volatile, influenced by a range of global economic factors, market sentiment, and geopolitical events.

One advantage of having a focused portfolio of projects, along with a highly experienced board and management team in mining, exploration, and capital markets, is the option open to Eastport to explore different scenarios that can best augment value on a project-by-project basis.

Our knowledge and understanding of our projects will increase significantly over the coming months, and these results will guide us in terms of the best strategy to continue building value for the company and our shareholders.